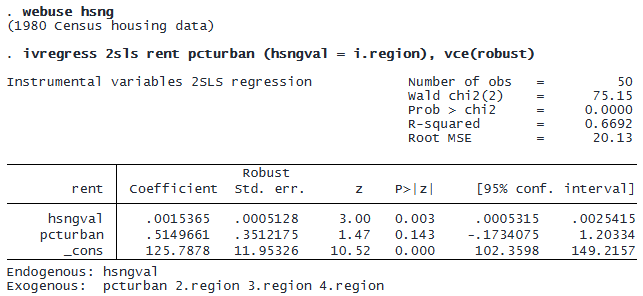

We are interested in modeling the average rental rate (rent) in each U.S. state as a function of average housing values (hsngval) and the proportion of the population living in urban areas (pcturban). Because average housing values are likely to be endogenous, we instrument hsngval using indicator variables for the region in which each state is located (i.region).

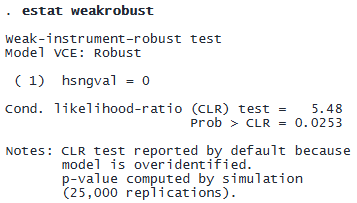

We suspect that our instruments for hsngval are weak. We can perform a test on the coefficient of hsngval that is robust to weak instruments by using estat weakrobust.

© Copyright 1996–2026 StataCorp LLC. All rights reserved.

estat weakrobust reports a CLR test, which is the default behavior when the model is overidentified (meaning there are more instruments than endogenous regressors). estat weakrobust has accounted for the fact that we have fit the model using a heteroskedasticity-robust variance–covariance estimate (VCE) and reported an appropriate heteroskedasticity-robust version of the CLR test.

We are less confident that the coefficient on hsngval is different from zero (Prob > CLR = 0.0253) compared with the results from ivregress (P>|z| = 0.003).

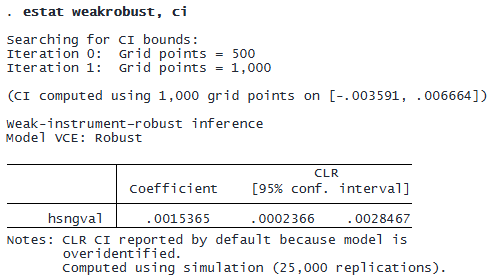

We can also request a confidence interval robust to weak instruments:

The CLR confidence interval of [.0002, .0028] is noticeably wider than the conventional confidence interval of [.0005, .0025] from the output of ivregress and comes closer to containing 0. Indeed, if we specified a confidence level of 99% by specifying the option level(99), 0 would be included in the confidence interval, and we would not rule out a zero coefficient on hsngval.